What Krishna’s chariot can teach you about your bank balance

I’m not a finance guru — just someone who got tired of the month-end scramble across five banking apps. This is the idea that helped me most, borrowed from a much older story than any budgeting app.

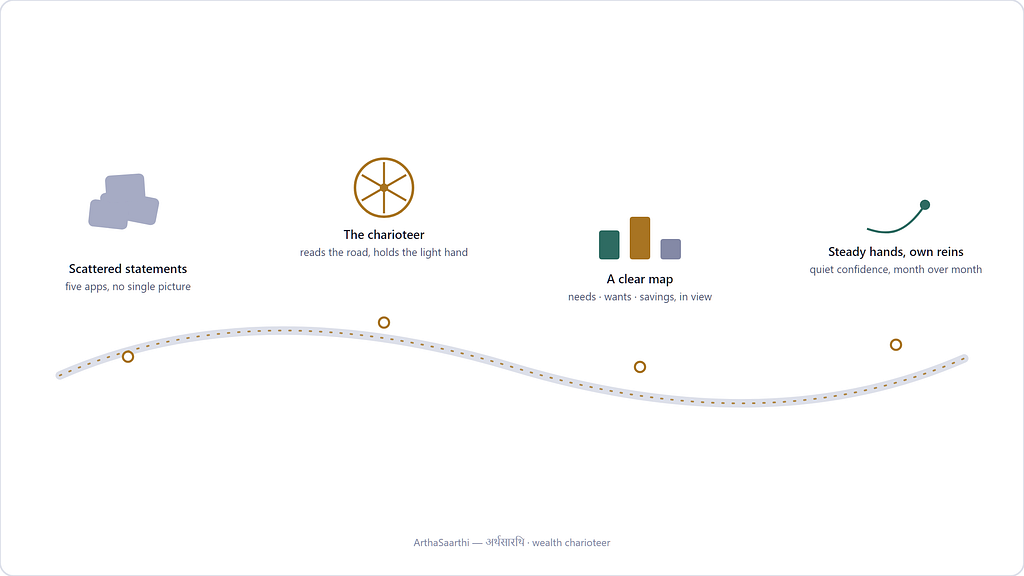

It’s the last week of the month. You open one banking app, then another, then a UPI history, then maybe a credit card statement — and somewhere between the fourth tab and the fifth, you give up trying to figure out exactly where the money went.

Not because you were reckless.

Just because it was scattered — a little here, a little there, across accounts that don’t talk to each other. That quiet, low-grade anxiety of “I know I earned enough, so where did it go?” is one of the most common and least talked-about kinds of money stress.

There’s an old idea, from the Bhagavad Gita, that’s stuck with me while thinking about this problem. Krishna serves as Arjuna’s charioteer in the story — but notice what he doesn’t do. He doesn’t seize the reins and drive the chariot himself. He sits beside Arjuna, reads the terrain, and helps him see the road clearly enough to steer it himself. That’s a surprisingly good model for what most of us actually want from help with our money. Not someone to take control. Someone who can see the whole road, so we can hold the reins with a little more confidence.

The problem isn’t overspending — it’s invisible spending

Most people who feel bad about their finances at month-end haven’t actually overspent in any dramatic way. What’s really happening is that spending is invisible — spread thin across five apps, three banks, and a stack of UPI payments that never quite get looked at together.

You can’t fix what you can’t see. The first job of any real financial “charioteer” isn’t to lecture you about discipline. It’s simply to gather the scattered road into one map you can actually look at.

There’s a saying that captures this better than any budgeting advice ever has: बूँद बूँद से घड़ा भरता है — “drop by drop, the pot fills.” Nobody tracks their spending perfectly. Nobody labels every single transaction the week it happens. But small, consistent drops of attention — a few minutes tagging expenses now and then — quietly accumulate into something you didn’t have before: a clear pot instead of a leaking one.

A compass, not a cage

Once the picture is visible, the next useful idea is simple: split spending into three buckets — needs, wants, and savings — roughly following what’s often called the 50/30/20 rule.

This isn’t a rulebook to obey perfectly. It’s a compass. Some months lean more toward needs, some allow more room for wants, and that’s fine. The value isn’t in hitting an exact number — it’s in having any honest sense of which direction you’re drifting, instead of flying blind.

This is close to another old idea from the Gita, sometimes called nishkama karma — doing the work without obsessively fixating on the outcome of every single instance of it. Applied to money, it looks like this: track consistently, review calmly, and don’t spiral over any one bad month. The picture that matters is the trend, not the single data point.

Judgment plus a little help beats either alone

Here’s the part that surprised me most: the best results didn’t come from handing everything over to automation, and they didn’t come from doing everything manually either. They came from a partnership. You glance at a transaction and label it — “that was groceries,” “that was rent” — and a bit of quiet automation fills in the gaps for everything you didn’t get to, using patterns from what you’ve already told it. Your judgment always has the final word. The automation’s only job is to make sure nothing falls through the cracks when you’re busy living your life instead of studying a spreadsheet.

And then, once a month, instead of a vague feeling of dread, you get something closer to a report card — a plain-language “financial health” snapshot. Not a scolding. Just an honest, calm read of where things stand, the way a doctor reads a check-up: here’s what’s healthy, here’s what needs a little attention, here’s what’s trending well.

Built the same way, fittingly

There’s a small bit of poetry in how this tool came to exist: it was built with the help of an AI coding assistant called Claude Code — not by handing over a wishlist and waiting for finished software to appear, but more like directing a capable apprentice who could open the files, try things, run them, and show the results, turn after turn. Every real decision — what the tool should actually do, what mattered, when something was truly done — stayed with the person building it. The AI did the hands-on work alongside them. A tool about not handing over your reins was, fittingly, built by someone who kept hold of theirs.

Holding your own reins

The point was never to hand your money over to an AI and stop thinking about it. It’s the opposite. The goal is to finally see the road clearly enough — where the money comes from, where it goes, what it’s quietly doing for your future — that you can hold the reins yourself, with a steadiness that comes from actually knowing the terrain instead of guessing at it.

A charioteer doesn’t drive for you. A good one just makes sure you can finally see where you’re going.

![]()

Everyone Needs a Charioteer for Their Money was originally published in Javarevisited on Medium, where people are continuing the conversation by highlighting and responding to this story.

This post first appeared on Read More